35 Common Financial Mistakes That Destroy Marriages

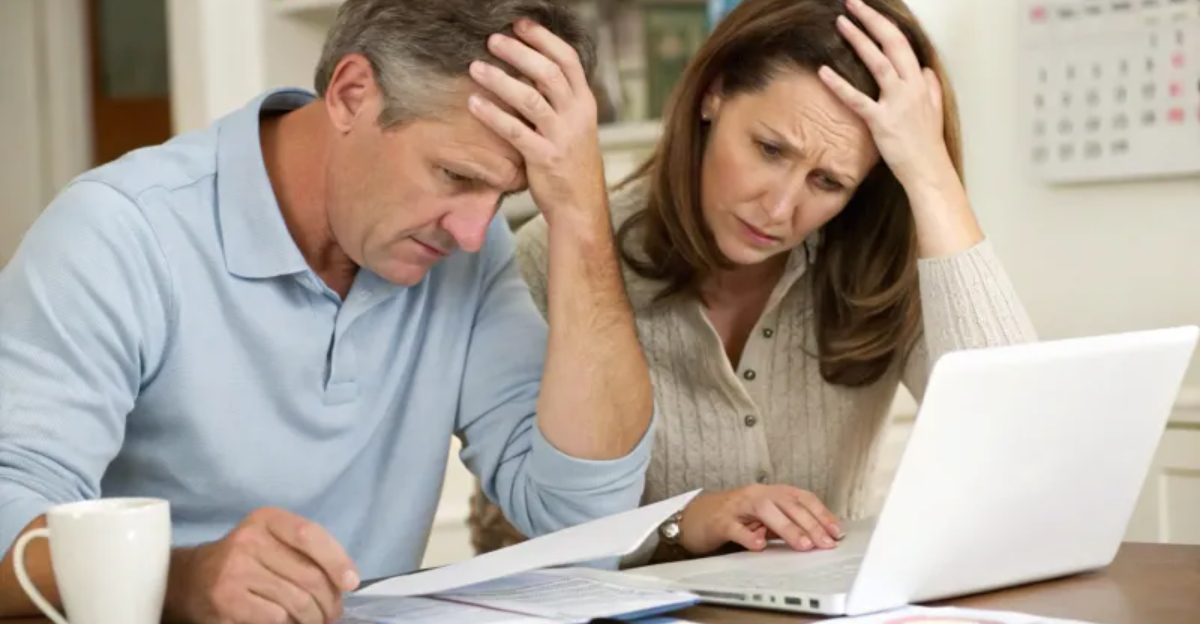

Financial disagreements are a leading cause of marital breakdowns, yet many couples overlook them until it’s too late.

As someone who understands the profound impact money has on relationships, I can tell you that ignoring financial issues in a marriage can be catastrophic.

It’s essential to approach these challenges with transparency, communication, and a willingness to find solutions together. By addressing common financial pitfalls, couples can build a more harmonious and financially secure marriage.

1. Keeping Financial Secrets

In any relationship, trust is paramount, and keeping financial secrets can erode that trust faster than you might think. When you hide debts, secret accounts, or expensive purchases, you plant the seeds of mistrust that can lead to significant marital discord. Transparency in finances is crucial; it’s about being open and honest about all monetary dealings. Imagine the relief and strength a relationship gains when both partners are on the same page financially.

Addressing this issue involves setting up regular financial ‘check-ins’ where both partners disclose financial statuses, debts, and expenditures. This practice fosters an environment of trust and mutual respect. Additionally, creating a shared financial goal can help align each partner’s priorities and make financial discussions less stressful.

If you find yourself struggling to disclose financial secrets, it might be helpful to talk to a financial counselor who can facilitate these conversations. Remember, the financial health of your marriage starts with honesty. By nurturing an open dialogue, you protect your relationship from the destructive power of financial secrets.

2. Spending Beyond Your Means

Living a lifestyle beyond your means is a temptation many couples face, especially in a society that equates happiness with material possessions. When you spend more than you earn, you set your marriage up for financial stress and conflict. It’s not just about the money; it’s about the impact it has on your relationship.

Creating and sticking to a realistic budget is a critical step in avoiding this pitfall. Take the time to evaluate your income versus your expenses and determine what’s truly necessary and what can be cut back. Prioritize needs over wants, and consider the long-term benefits of financial stability over short-term gratification.

Engage in open conversations with your partner about financial priorities and set limits together. This cooperative approach ensures mutual understanding and helps prevent future misunderstandings. Remember, financial freedom comes not from having more, but from needing less.

3. Failing to Create a Budget

Without a budget, financial chaos reigns, leading to stress and arguments over money. Many couples underestimate the power of a well-constructed budget, thinking it’s restrictive rather than liberating. But the truth is, a budget is your roadmap to financial freedom and marital harmony.

Creating a budget involves sitting down with your partner and assessing your monthly income and expenses. Identify essential expenses and areas where you can cut back. Use tools like budgeting apps or simple spreadsheets to track your spending and keep each other accountable.

Sticking to a budget requires discipline and teamwork. It’s not just about numbers; it’s about building a future together. Regular budget reviews can help you adapt to changes in income or unexpected expenses and keep you aligned with your financial goals. By embracing budgeting as a couple, you lay the foundation for a stable financial future.

4. Not Setting Financial Goals Together

When couples don’t set financial goals together, they drift apart financially and emotionally. Without shared objectives, each partner may pursue separate financial paths, leading to misunderstandings and resentment. Joint goals bring unity and purpose to a relationship.

Start by discussing your individual financial dreams and finding common ground. Whether it’s saving for a house, planning for retirement, or setting up an emergency fund, aligning on these goals strengthens your partnership. It’s important to revisit these goals regularly and adjust them as your circumstances change.

By achieving these goals together, you not only secure your financial future but also strengthen your emotional bond. Working towards a common objective fosters cooperation, understanding, and mutual support. Remember, in the realm of marriage, teamwork makes the dream work.

5. Avoiding Money Conversations

Money conversations can be uncomfortable, but avoiding them only amplifies financial issues. Many couples dodge these discussions out of fear of conflict or misunderstanding, but in doing so, they allow small problems to fester into significant issues.

Approach money talks with openness and a willingness to understand each other’s perspectives. Set aside time each month to discuss finances, ensuring both partners have an equal voice in the conversation. Transparency is key; discuss debts, future expenses, and financial fears without judgment.

Practicing active listening and empathy creates a safe space for these conversations. Remember, the goal is not to win an argument but to find a solution together. By regularly engaging in these discussions, you prevent financial issues from becoming insurmountable and strengthen your partnership.

6. Relying on One Income

Depending solely on one income can be risky, especially in today’s uncertain economic climate. When a marriage relies on a single source of income, the couple is vulnerable to financial instability if that income is lost. This reliance can also place undue stress on the earning partner, leading to resentment and tension.

To mitigate this risk, explore ways to diversify your income streams. This could involve one partner taking on a part-time job or starting a side hustle. Additionally, consider building an emergency fund that can cover expenses for several months in case of an unexpected job loss.

Discussing career goals and financial responsibilities openly ensures both partners are on the same page and prepared for potential changes. By diversifying income and planning for uncertainties, you safeguard your marriage against financial disruption.

7. Not Saving for Emergencies

Emergencies are inevitable, and not having savings set aside can strain a marriage during crises. An emergency fund is not a luxury; it’s a necessity that provides peace of mind and financial security. Without it, unexpected expenses can lead to debt and increased marital stress.

Start by setting a realistic savings goal, aiming to cover three to six months of living expenses. Open a separate savings account dedicated solely to emergency funds to avoid the temptation of spending it on non-essentials.

Regularly contribute to this fund, even if it’s a small amount each month. The key is consistency and commitment from both partners. Having a financial cushion not only eases the burden during tough times but also strengthens your marriage by reducing money-related worries.

8. Letting Financial Stress Dominate Arguments

When financial stress infiltrates every argument, it becomes the root of all conflict, overshadowing other issues. This dynamic creates a hostile environment where money is blamed for every disagreement, damaging communication and emotional connection.

Recognize the signs of financial stress and address them directly rather than letting them bleed into unrelated arguments. Set boundaries for discussions about finances, choosing a specific time and place to talk about money issues calmly and constructively.

Couples counseling can also be beneficial in learning how to separate financial stress from personal grievances. By keeping financial discussions focused and respectful, you prevent them from taking over your marriage and preserve the health of your relationship.

9. Ignoring Credit Scores

Credit scores play a crucial role in your financial health, yet many couples ignore them until it’s too late. A poor credit score can affect your ability to get loans, rent apartments, or secure favorable interest rates, impacting your financial future together.

Regularly check your credit scores and discuss any discrepancies or issues with your partner. Understanding what affects your credit score empowers you to make informed decisions and improve it over time.

Working together to maintain or improve your credit scores strengthens your financial standing as a couple. It’s an ongoing process that requires communication, discipline, and shared responsibility. By taking credit scores seriously, you lay the groundwork for a stable financial future.

10. Combining Finances Prematurely

Merging finances is a significant step in any relationship, and doing it prematurely can lead to confusion and resentment. Each partner may have different spending habits and financial philosophies, so it’s important to approach this transition with patience and understanding.

Begin by discussing your financial histories, values, and expectations before combining accounts. Consider starting with a joint account for shared expenses while maintaining individual accounts for personal spending. This approach allows for a gradual adjustment to managing money together.

Clear communication and setting boundaries are essential in navigating this change. Regularly review your financial situation as a couple, ensuring both partners have equal input and control. By taking a measured approach, you build a financial partnership that respects individual autonomy and promotes collaboration.

11. Neglecting Retirement Planning

Retirement may seem distant, but neglecting to plan for it can leave you unprepared and stressed later in life. Failing to prioritize retirement savings leads to a future filled with financial uncertainty and dependence on others.

Start by discussing retirement goals with your partner, considering the lifestyle you envision and the financial resources required to support it. Explore retirement savings options like 401(k)s or IRAs, and contribute regularly to these accounts.

Revisit your retirement plan annually, adjusting contributions and investments as needed to stay on track. By taking retirement planning seriously now, you ensure a comfortable and secure future for both you and your partner, free from financial worries.

12. Overextending with Debt

Debt can be a silent killer in marriages, especially when it spirals out of control. Overextending with debt not only affects your financial health but also creates tension and mistrust between partners.

To manage debt effectively, start by listing all outstanding debts and prioritizing them based on interest rates and urgency. Consider debt consolidation or repayment strategies that suit your financial situation.

Engage in open discussions with your partner about debt management and create a plan to tackle it together. This collaborative approach ensures both partners are committed to reducing debt and improving financial stability. By addressing debt head-on, you protect your marriage from its destructive effects and build a brighter financial future.

13. Ignoring Inflation Impact

Inflation affects purchasing power, yet many couples overlook its impact on their finances. Ignoring inflation can lead to budgeting inaccuracies and financial strain, as the cost of living continues to rise.

To combat inflation, regularly review and adjust your budget to reflect current prices for goods and services. Consider investing in assets that historically outpace inflation, such as stocks or real estate.

Discuss inflation’s impact as a couple and explore strategies to mitigate its effects on your long-term financial plans. By staying informed and proactive, you safeguard your finances against inflation’s erosive effects, ensuring stability for your marriage.

14. Skipping Insurance Coverage

Insurance is a safety net that many couples overlook, often until it’s too late. Skipping insurance coverage can lead to financial devastation in the event of a medical emergency, accident, or natural disaster.

Evaluate your insurance needs as a couple, considering health, life, auto, and property insurance. Choose coverage that suits your lifestyle and financial situation, ensuring you’re protected against unexpected events.

Regularly review your insurance policies and make adjustments as your circumstances change. By prioritizing insurance, you provide financial security and peace of mind for your marriage, protecting against unforeseen challenges.

15. Not Keeping Financial Records

Maintaining accurate financial records is essential for effective money management, yet many couples neglect this practice. Without clear records, managing expenses, tracking savings, and preparing for taxes become daunting tasks.

Implement a system for organizing financial documents, whether digital or physical, and ensure both partners have access to it. Regularly update records to reflect current financial transactions and changes.

By keeping your financial records in order, you simplify budgeting, tax preparation, and decision-making processes. This practice promotes transparency and accountability within your marriage, fostering a collaborative financial partnership.

16. Mismanaging Joint Accounts

Joint accounts can simplify shared expenses, but mismanagement leads to conflict and financial disarray. Issues like unauthorized withdrawals, overdrafts, or untracked spending can strain the relationship.

Establish clear guidelines for using joint accounts, ensuring both partners understand the terms of deposits and withdrawals. Regularly review account statements together to monitor spending and prevent discrepancies.

Communication is key; discuss any concerns about joint account management openly and constructively. By maintaining transparency and mutual respect, you prevent joint accounts from becoming a source of tension and instead make them a tool for financial harmony.

17. Valuing Possessions Over Relationships

When possessions become more important than the relationship, financial priorities are skewed, leading to emotional distance. Valuing material wealth over emotional connection creates a divide that can be challenging to bridge.

Reassess your values as a couple, focusing on experiences and shared goals rather than material accumulation. Discuss what truly matters and how your financial resources can support those priorities.

Building a marriage on a foundation of shared values rather than possessions fosters a deeper connection and mutual respect. By prioritizing the relationship over material wealth, you create a lasting bond that withstands financial challenges.

18. Underestimating the Cost of Children

Having children is a joyous milestone, but many couples underestimate the financial commitment involved. From diapers to education, the costs can quickly add up, leading to financial strain and stress.

Plan for the financial impact of children by creating a comprehensive budget that accounts for all potential expenses. Consider opening a savings account dedicated to childcare costs, and explore options like education savings plans.

Discuss family planning and financial responsibilities openly with your partner. By preparing for the costs of children, you ensure your marriage remains strong and supportive, capable of handling the financial challenges ahead.

19. Not Investing in Financial Education

Financial literacy is essential for managing money effectively, yet many couples overlook the importance of ongoing financial education. Without understanding financial principles, making informed decisions becomes challenging.

Invest in financial education as a couple by taking courses, reading books, or attending workshops on personal finance topics. The knowledge gained empowers both partners to make informed financial decisions and plan for the future.

Regularly update your financial knowledge to stay informed about changing economic conditions and financial opportunities. By prioritizing financial education, you strengthen your marriage’s financial foundation, ensuring a secure and prosperous future together.

20. Failing to Address Financial Infidelity

Financial infidelity, or hiding financial activities from your partner, can be devastating to a marriage. This breach of trust goes beyond money, affecting emotional intimacy and stability.

Address financial infidelity by fostering open communication and honesty. Create an environment where both partners feel safe discussing financial mistakes or concerns without fear of judgment.

Consider seeking professional counseling to rebuild trust and establish healthy financial habits. By addressing financial infidelity head-on, you repair the damage and strengthen the foundation of trust within your marriage, paving the way for a more secure future.

21. Ignoring Tax Implications

Ignoring tax implications can lead to unexpected liabilities and financial strain. Many couples overlook the importance of understanding tax responsibilities and planning accordingly.

Stay informed about tax laws and regulations that affect your financial situation. Consider consulting with a tax professional to maximize deductions and credits, ensuring you comply with tax requirements.

By addressing tax implications proactively, you avoid surprises and maintain financial stability. Open discussions about tax responsibilities build transparency and trust within your marriage, avoiding unnecessary stress and conflict.

22. Not Prioritizing Debt Repayment

Failing to prioritize debt repayment can lead to a never-ending cycle of financial stress. When couples don’t address debt strategically, it accumulates, becoming a burden that affects every aspect of life.

Create a plan to tackle debt by identifying high-interest obligations and focusing on them first. Explore strategies like the snowball or avalanche methods, and adjust your budget to allocate additional funds towards debt repayment.

Regularly review your progress and celebrate milestones together. By prioritizing debt repayment, you alleviate stress and build a stronger financial foundation for your marriage, setting the stage for future success.

23. Overlooking Partner’s Financial Habits

Ignoring or dismissing your partner’s financial habits can lead to misunderstandings and conflict. Each partner brings their own financial history and behavior to the relationship, which can clash without open communication.

Discuss your financial habits and histories with your partner, acknowledging differences and finding common ground. Respect each other’s perspectives and work together to create a financial strategy that accommodates both partners’ needs.

By understanding and accepting each other’s financial habits, you foster a harmonious partnership that leverages your individual strengths. This approach ensures a balanced and respectful financial relationship, avoiding unnecessary conflict.

24. Relying Solely on Credit Cards

Relying solely on credit cards for expenses can lead to debt accumulation and financial instability. This reliance often masks underlying financial issues and creates a false sense of security.

Create a budget that prioritizes cash flow management, reducing dependence on credit cards for everyday expenses. Consider using credit cards strategically, focusing on building credit and earning rewards without incurring debt.

Discuss alternatives to credit card reliance with your partner, such as emergency fund savings or debit card usage. By reducing credit card dependency, you improve financial stability and protect your marriage from the pitfalls of debt.

25. Failing to Adjust Financial Plans

Financial plans are not static; they require regular review and adjustment to reflect life changes and economic shifts. Failing to update plans can lead to missed opportunities and financial misalignment.

Schedule regular financial check-ins with your partner to assess your current situation and goals. Adjust plans to accommodate changes in income, expenses, or priorities, ensuring alignment with your long-term vision.

By keeping financial plans current, you stay proactive and adaptable, ready to seize opportunities and navigate challenges. This flexibility strengthens your marriage’s financial resilience, promoting stability and growth.

26. Not Considering Long-Term Care Costs

Long-term care costs are often overlooked, yet they can have a substantial financial impact later in life. Failing to plan for these expenses can lead to financial stress and difficult decisions.

Discuss long-term care options with your partner, exploring insurance or savings strategies to cover potential costs. Consider the emotional and financial implications, ensuring both partners are prepared for future needs.

By planning for long-term care, you protect your marriage from financial strain and ensure that both partners receive the care they need. This foresight provides peace of mind and security for your future together.

27. Not Diversifying Investments

Investing is crucial for building wealth, but failing to diversify can lead to significant financial risk. Concentrating investments in a single asset class exposes you to volatility and potential losses.

Evaluate your investment portfolio with your partner, ensuring a diverse mix of assets that align with your risk tolerance and financial goals. Consider stocks, bonds, real estate, and other investment vehicles to spread risk.

By diversifying investments, you protect your financial future from market fluctuations and create a more stable foundation for growth. This strategy enhances your marriage’s financial security, allowing you to pursue your dreams with confidence.

28. Ignoring Estate Planning

Estate planning is often neglected, yet it’s essential for protecting your assets and ensuring your wishes are honored. Without it, loved ones may face legal challenges and financial uncertainty.

Discuss estate planning with your partner, exploring wills, trusts, and other tools to secure your estate. Consider the needs of dependents and potential tax implications, ensuring a comprehensive plan.

Regularly update estate plans to reflect life changes and evolving priorities. By prioritizing estate planning, you provide clarity and security for your family, strengthening your marriage’s financial foundation.

29. Not Seeking Professional Financial Advice

Managing finances can be complex, and many couples benefit from professional guidance. Failing to seek financial advice leaves you without expert insights and strategies to optimize your financial situation.

Consider consulting a financial advisor to gain a clear understanding of your financial landscape. They can provide tailored advice on budgeting, investments, retirement planning, and more, helping you make informed decisions.

By seeking professional advice, you enhance your financial knowledge and confidence, ensuring your marriage remains financially healthy and resilient. This proactive approach supports your long-term goals and safeguards your financial future.

30. Failing to Discuss Financial Roles

Defining financial roles within a marriage is crucial for efficiency and harmony. When roles are unclear, tasks can be neglected, leading to financial disorganization and conflict.

Discuss and assign financial responsibilities based on each partner’s strengths and availability. Whether it’s budgeting, bill payments, or investment tracking, clear roles ensure accountability and prevent misunderstandings.

Regularly review and adjust roles as needed, fostering a cooperative and supportive financial relationship. By defining financial roles, you promote teamwork and clarity, strengthening your marriage’s financial health.

31. Collecting Rare, Expensive Niche Hobbies

Everyone loves a good hobby, but when niche collectibles become an obsession, it’s a different ball game. Imagine spending thousands on vintage typewriters only to realize they’re taking over your attic! While hobbies are essential for personal happiness, when they turn into pricey endeavors, they can strain a marriage.

Balancing personal interests with a partner’s financial expectations is crucial. Transparent communication about spending limits can prevent resentment. It’s all about finding harmony between passion and practicality, ensuring hobbies enrich lives without draining savings. Couples should periodically review their spending to keep things in check.

32. Investing in a Fantasy Business Venture

Who hasn’t dreamed of a whimsical business venture? A unicorn farm, perhaps? The thrill of creating something magical can be enticing but investing in fantastical ideas without concrete plans can lead to financial distress.

Couples might find themselves amidst clouds of imagination, overlooking essential business strategies. To maintain financial health, it’s vital to ground dreamy ventures in reality. Research, feasibility studies, and expert consultations are critical steps. Practicality doesn’t mean abandoning dreams, but rather shaping them into sustainable realities. Open dialogues about potential financial impacts can ensure dreams don’t turn into nightmares.

33. Betting Big on Unknown Currencies

Cryptocurrencies can be thrilling, yet speculative investments. Venturing into obscure digital currencies might seem adventurous but can be a financial quagmire. The allure of rapid gains often overshadows the risks involved.

Couples diving into this volatile market without understanding can face unexpected losses. It’s essential to research, diversify investments, and assess risk tolerance. Financial missteps in this arena can lead to stress and disagreements, impacting relationships. Transparent discussions about investment goals and strategies can mitigate risks, ensuring that the journey into digital currencies is informed and harmonious.

34. Overlooking Small, Recurring Expenses

Small expenses might seem insignificant, but over time, they add up and can impact a couple’s financial health. Subscriptions, daily coffee runs, and frequent dining out are common culprits that can silently drain resources.

Couples need to regularly audit their small expenses to identify areas where they can cut back. Setting a monthly limit for discretionary spending can also help in managing these recurring costs. This habit not only saves money but also promotes accountability and transparency in financial matters.

35. Not Planning for Major Life Changes

Life is full of unexpected turns, and failing to plan for major changes like having a baby, moving, or changing jobs can be detrimental. Such oversights can place immense stress on a relationship, as financial strain mounts without a clear plan in place.

Couples should regularly discuss potential life changes and prepare a financial roadmap. This includes saving for future events and setting realistic financial goals. By doing so, they establish a safety net that ensures both partners feel secure and supported through life’s transitions.